What is an FHA Home Loan?

FHA home loans are insured by the Federal Housing Administration (FHA), and can only be provided by lenders approved by the FHA. This type of mortgage has a fixed term length of either 15 or 30 years. It’s a popular choice among first-time homebuyers in Southwest Florida, as well as buyers with limited savings or lower credit scores.

When purchasing a home, you might be responsible for certain out-of-pocket expenses like loan origination fees, appraisal costs, and attorney fees. One of the advantages of an FHA home loan is that the seller, home builder, or lender can cover some of these closing costs on your behalf.

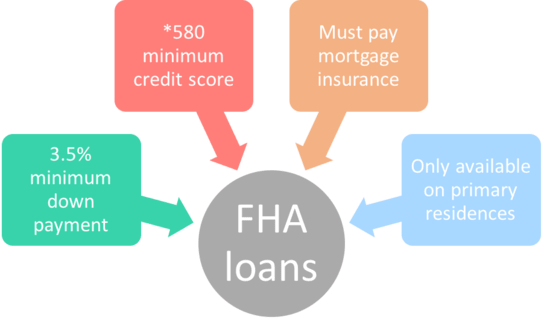

The minimum down payment (3.5%) and credit score requirements (at least 580) of FHA loans are lower than that of many conventional loans. And unlike conventional mortgages, 100% of your down payment can be a gift. This gift can come from any of the following:

- The borrower’s relative.

- An employer or labor union.

- A close friend.

- A charitable organization.

- A governmental agency or public entity that has a program providing home ownership assistance.

If your credit score is between 500 and 579, you still can qualify for this kind of loan; however, you’ll have to make a larger down payment.

Generally speaking, the lower your credit score and down payment, the higher the interest rate you’ll pay on the mortgage.

Mortgage Insurance Premiums

Borrowers in Southwest Florida who obtain an FHA loan must pay FHA mortgage insurance (this protects the lender from a loss if you default on the loan). You’re required to pay two types of mortgage insurance premiums—an Upfront Mortgage Insurance Premium (UFMIP) and an Annual MIP (charged monthly). This is different from government-insured loans, where you have to pay private mortgage insurance (PMI).

As of 2020, the UFMIP is equal to 1.75% of the base loan amount. It can either be rolled into the loan or paid at the time of closing. As for Annual MIP, your monthly payments will range from 0.45% to 1.05% of the base loan amount, depending on factors such as length of the loan, the base amount, and the original loan-to-value ratio (LTV).

If you start with a down payment of less than 10%, you’ll continue to pay mortgage insurance for the duration of the loan. Those with 10% down payments will pay FHA mortgage insurance for 11 years.

How to Qualify For a FHA Loan in Southwest Florida

- Have a debt-to-income ratio (DTI) of no more than 50%. This means that your total monthly debt payments can’t be more than 50% of your pretax income (includes debts that you aren’t actively paying).

- Pay the upfront mortgage insurance premium (UFMIP). This is usually equal to 1.75% of the base loan amount.

- Have bank statements for the last 30 days. You’ll also need to provide documentation for any deposits made during that time (usually pay stubs).

- Must have a steady job history (if self-employed, have two years of successful self-employment history; this should be documented by a current year-to-date balance sheet, tax returns, and a profit and loss statement).

- Must be at least two years out of bankruptcy, unless you can prove that the bankruptcy was due to circumstances beyond your control.

- Must be at least three years removed from any foreclosures.

- Have a valid social security number.

- Have U.S. citizenship and be of legal age.

FHA approved lenders use a program called Desktop Underwriter (DU) for mortgage approval. DU looks at the potential borrower’s debt ratio, reserves and credit score to make an automated credit decision. Southwest Florida lenders can also add their own rules, also known as overlays on top of the minimum requirements listed above. As each lender sets their own rates and terms, comparison shopping is important in this market.

Types of FHA Loans

- Traditional – used to finance primary residences.

- Home Equity Conversion – (reverse mortgage) allows homeowners 62 years of age and older to exchange their home equity for cash while still retaining title to the home. Funds can either be withdrawn as a fixed monthly amount or as a line of credit.

- 203(k) Program – includes extra funds to pay for repairs and renovations to the Southwest Florida house. For this type of loan, the property may undergo two separate appraisals: an “as is” appraisal that evaluates its current state, and an “after improved” appraisal estimating the value after the work/renovations are finished.

- Energy Efficient Program – includes extra funds to pay for energy-efficient home improvements (could potentially lower the cost of your utility bills).

- Section 245(a) – a graduated payment mortgage (GPM) with reduced initial monthly payments that increase over time, and a growing equity mortgage (GEM) where fixed increases in monthly principal payments result in shorter loan terms. This program is for borrowers who anticipate an increase in income.